Understanding Qualified Opportunity Funds: A Comprehensive Guide

How QOFs Enable Tax-Deferred Investment in Underserved Communities

Qualified Opportunity Funds (QOFs) represent one of the most significant tax incentive programs created in recent years, offering investors the ability to defer—and potentially eliminate—capital gains taxes while simultaneously investing in economically distressed communities across the United States.

What Are Qualified Opportunity Funds?

A Qualified Opportunity Fund is an investment vehicle established under the Tax Cuts and Jobs Act of 2017. QOFs are designed to encourage long-term investments in low-income urban and rural communities designated as Qualified Opportunity Zones.

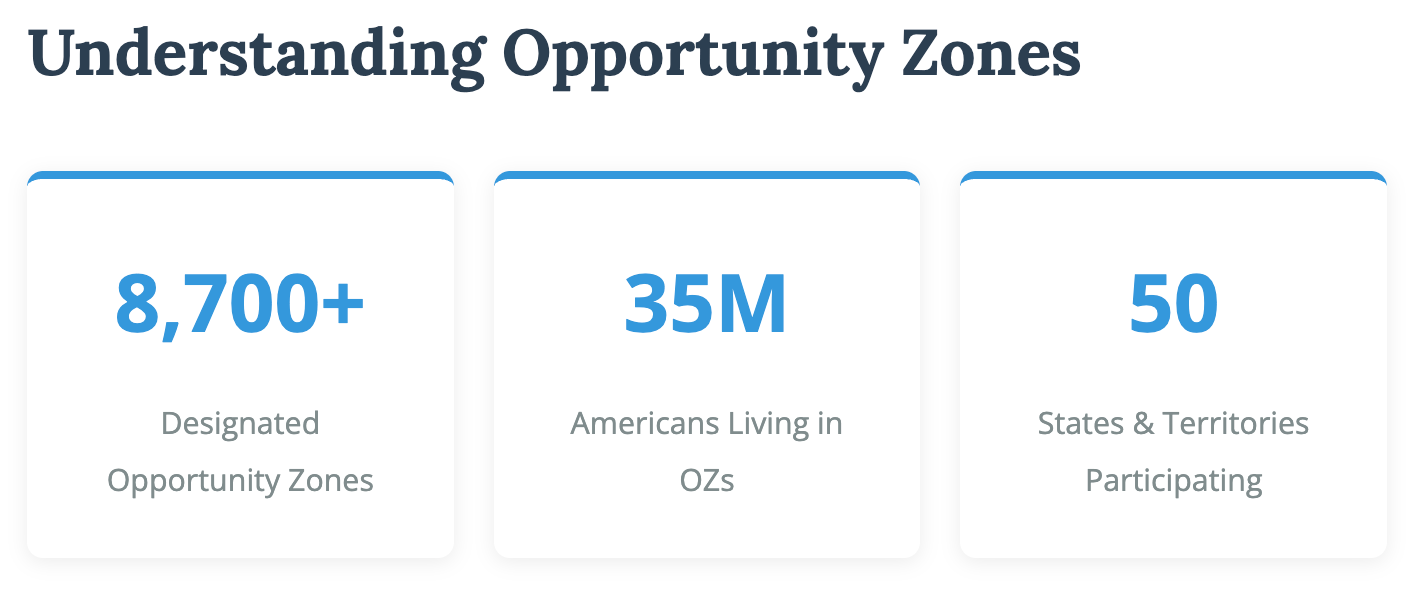

The program creates a powerful alignment of interests: investors receive substantial tax benefits while capital flows into communities that have traditionally struggled to attract investment. As of 2026, there are more than 8,700 designated Opportunity Zones across all 50 states, the District of Columbia, and U.S. territories.

The Three-Tier Tax Benefit Structure

QOFs offer a tiered system of tax advantages that reward patient capital:

How the Timeline Works

Who Should Consider QOFs?

Qualified Opportunity Funds are particularly attractive for certain investor profiles:

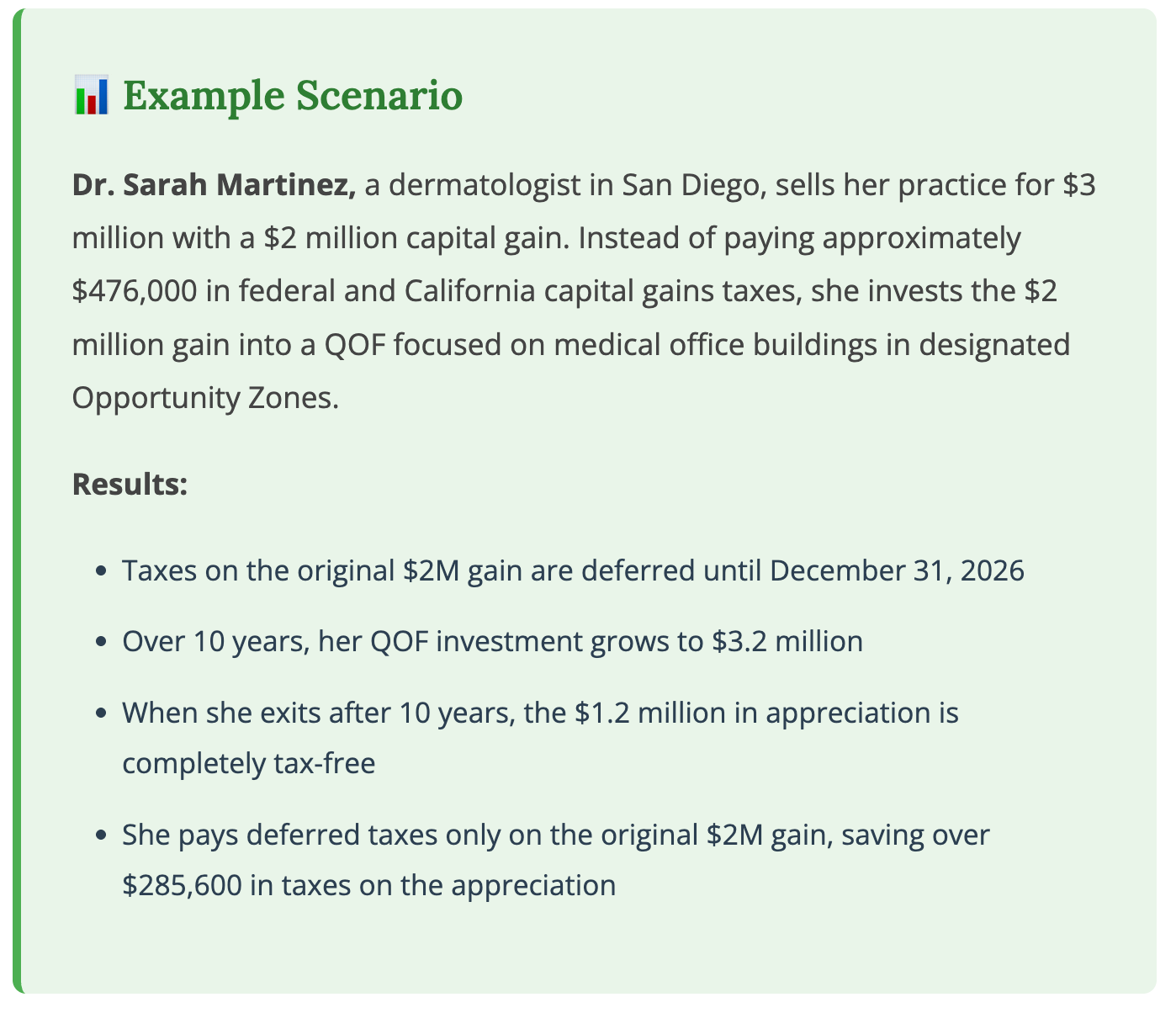

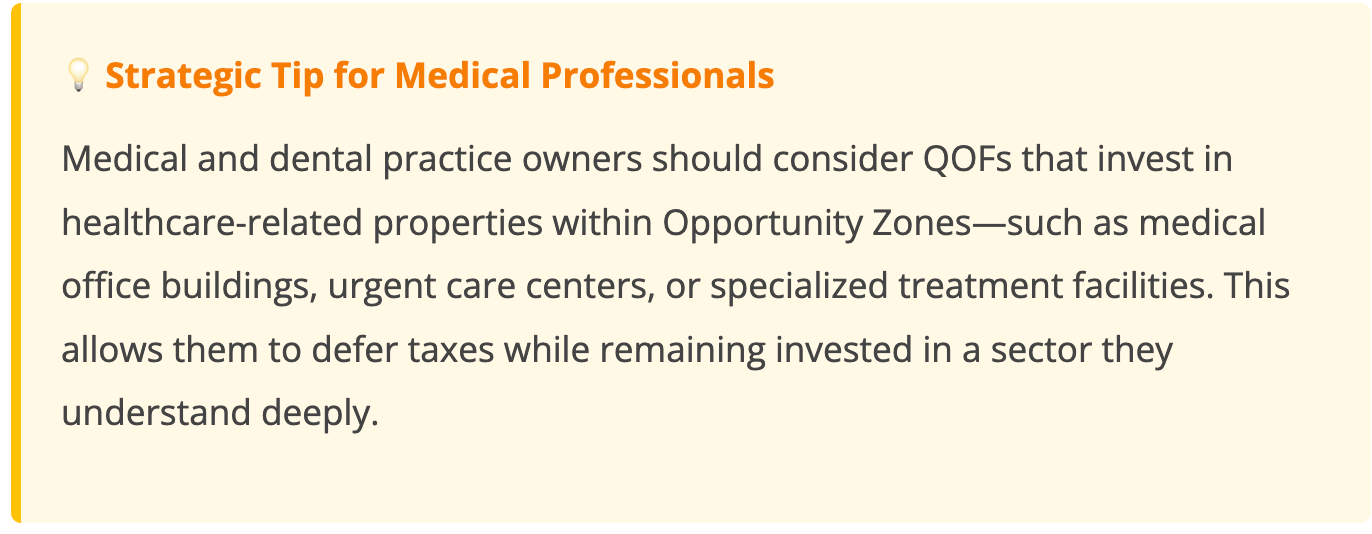

Medical and Dental Practice Owners

Physicians and dentists who sell their practices often face substantial capital gains. Rather than paying taxes immediately, they can reinvest proceeds into a QOF, defer the tax until 2026, and potentially build a tax-free retirement portfolio if held for 10 years.

Real Estate Investors

Property owners who have exhausted their 1031 exchange options or are looking for additional flexibility find QOFs attractive. Unlike 1031 exchanges, QOF investments don’t require like-kind property—any capital gain can be invested.

Business Owners and Executives

Those selling businesses or exercising stock options with significant gains can use QOFs to defer taxation while diversifying into real estate or operating businesses in Opportunity Zones.

High-Net-Worth Families

Families with concentrated wealth in appreciated assets can use QOFs as part of broader estate planning and wealth transfer strategies, particularly when combined with defined benefit pension plans and other tax-advantaged vehicles.

Opportunity Zones are census tracts designated by state governors and certified by the U.S. Treasury Department. To qualify, areas must meet specific criteria for low-income status based on poverty rates and median family income.

These zones exist in both urban and rural areas, spanning major cities like Los Angeles and New York as well as small towns throughout the country. Many zones are experiencing significant revitalization, while others remain in early stages of development.

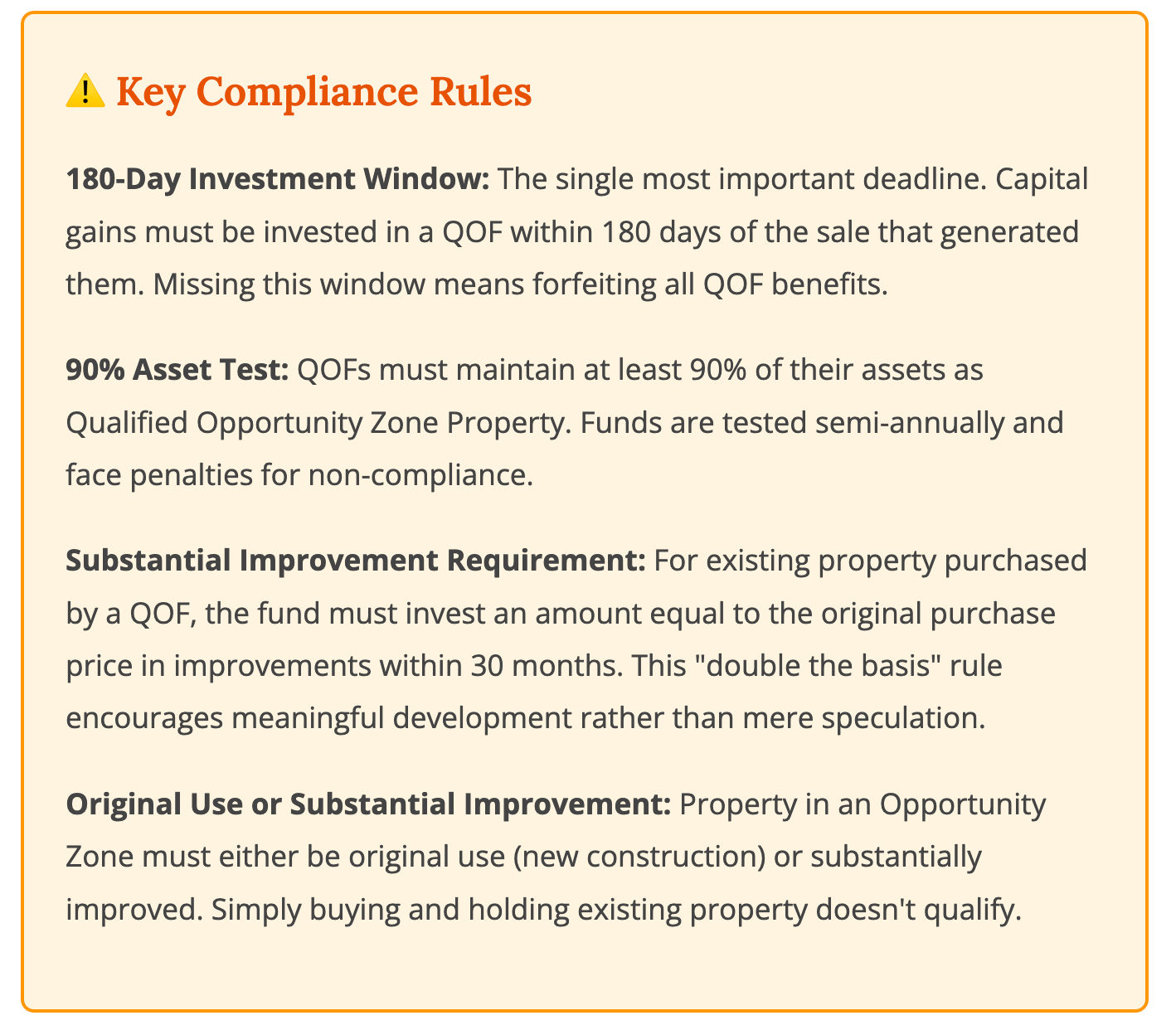

Critical Requirements and Compliance

Investment Structures and Strategies

QOFs typically invest through two primary strategies:

Real Estate Development

The most common QOF strategy involves developing or substantially rehabilitating real estate in Opportunity Zones. Projects range from multifamily housing and retail centers to medical office buildings and mixed-use developments. Real estate QOFs appeal to investors seeking tangible assets and predictable cash flows.

Operating Businesses

QOFs can also invest in qualifying businesses located in Opportunity Zones. These “Qualified Opportunity Zone Businesses” (QOZBs) must derive at least 50% of their gross income from active conduct of business within the zone and meet specific property and business requirements.

Risks and Considerations

While QOFs offer compelling tax benefits, investors should carefully evaluate several risk factors:

Illiquidity

To realize the maximum tax benefits, investors must hold QOF investments for 10 years. This requires a long-term commitment and tolerance for illiquidity. Early exit means forfeiting the permanent appreciation exclusion.

Investment Risk

Tax benefits don’t eliminate investment risk. QOFs invest in economically distressed areas that may face development challenges, market volatility, or slower-than-expected growth. Due diligence on the fund manager, investment strategy, and specific projects is essential.

Regulatory Complexity

QOF regulations are complex and continue to evolve. The IRS has issued multiple rounds of guidance, and compliance requires careful attention to timing, documentation, and ongoing reporting requirements.

December 2026 Deadline

All deferred gains must be recognized by December 31, 2026, regardless of the QOF investment’s status. Investors should plan for this tax liability and ensure they have liquidity to pay the deferred taxes.

"The most powerful aspect of QOFs isn't the temporary deferral—it's the permanent exclusion of appreciation after 10 years. This transforms capital gains that would have been taxed at 20-37% into completely tax-free wealth." - Robert Mowry, Partner at of QOF

Integration with Retirement and Estate Planning

For medical professionals and business owners, QOFs work particularly well when integrated with other sophisticated planning strategies:

Defined Benefit Pension Plans

High-income physicians can combine large, tax-deductible contributions to defined benefit pension plans with QOF investments. This creates a “double benefit”: immediate tax deductions reduce current income while deferred capital gains reduce future tax liability.

Estate Planning

QOF investments held until death receive a step-up in basis, potentially eliminating both the deferred gain and any appreciation. This makes QOFs attractive for older investors who may not live to see the 10-year exclusion but want to defer taxes during their lifetime.

Charitable Strategies

Combining QOF investments with charitable remainder trusts or donor-advised funds can create additional tax efficiency, particularly for investors with significant philanthropic goals.

Due Diligence and Fund Selection

Choosing the right QOF requires thorough evaluation:

Track Record: Examine the fund manager’s experience with both the asset class (real estate or operating businesses) and the specific geographic markets where they invest.

Investment Strategy: Understand whether the fund focuses on development, rehabilitation, or operating businesses. Each carries different risk-return profiles and timelines.

Geographic Focus: Evaluate the specific Opportunity Zones where the fund invests. Not all zones offer equal prospects for appreciation and economic development.

Fee Structure: QOFs typically charge management fees and may include performance fees. Understand the total fee burden and how it affects net returns.

Exit Strategy: Confirm the fund has a clear plan for providing liquidity at the 10-year mark when the maximum tax benefits are realized.

Compliance Expertise: Verify that the fund manager has dedicated legal and tax resources to ensure ongoing compliance with complex QOF regulations.

Conclusion: A Powerful Tool for Patient Capital

Qualified Opportunity Funds represent a unique convergence of tax policy, economic development, and investment opportunity. For investors with significant capital gains—particularly medical professionals selling practices, real estate investors, and business owners—QOFs offer a compelling structure to defer taxes while building long-term, tax-free wealth.

The program’s most valuable benefit—permanent exclusion of appreciation after 10 years—rewards patient investors willing to commit capital for the long term. However, the complexity of regulations, illiquidity requirements, and investment risks mean that QOFs are not suitable for everyone.

Success with QOFs requires three elements: significant capital gains to defer, a long-term investment horizon of at least 10 years, and careful selection of well-managed funds investing in promising Opportunity Zones. When these conditions align, QOFs can be one of the most tax-efficient investment structures available under current law.

As with any sophisticated tax and investment strategy, consultation with qualified tax advisors, financial planners, and legal counsel is essential before making QOF investments. The potential benefits are substantial, but only when implemented correctly within a comprehensive financial plan.