The QOF Timeline: Your 10-Year Path to Tax-Free Wealth

Understanding exactly what happens at each milestone of your Qualified Opportunity Fund investment

When you invest in a Qualified Opportunity Fund, you’re not just making an investment—you’re starting a carefully structured timeline that can lead to completely tax-free appreciation. But this journey has specific milestones, critical deadlines, and increasingly valuable benefits as time passes.

Let me walk you through exactly what happens, step by step.

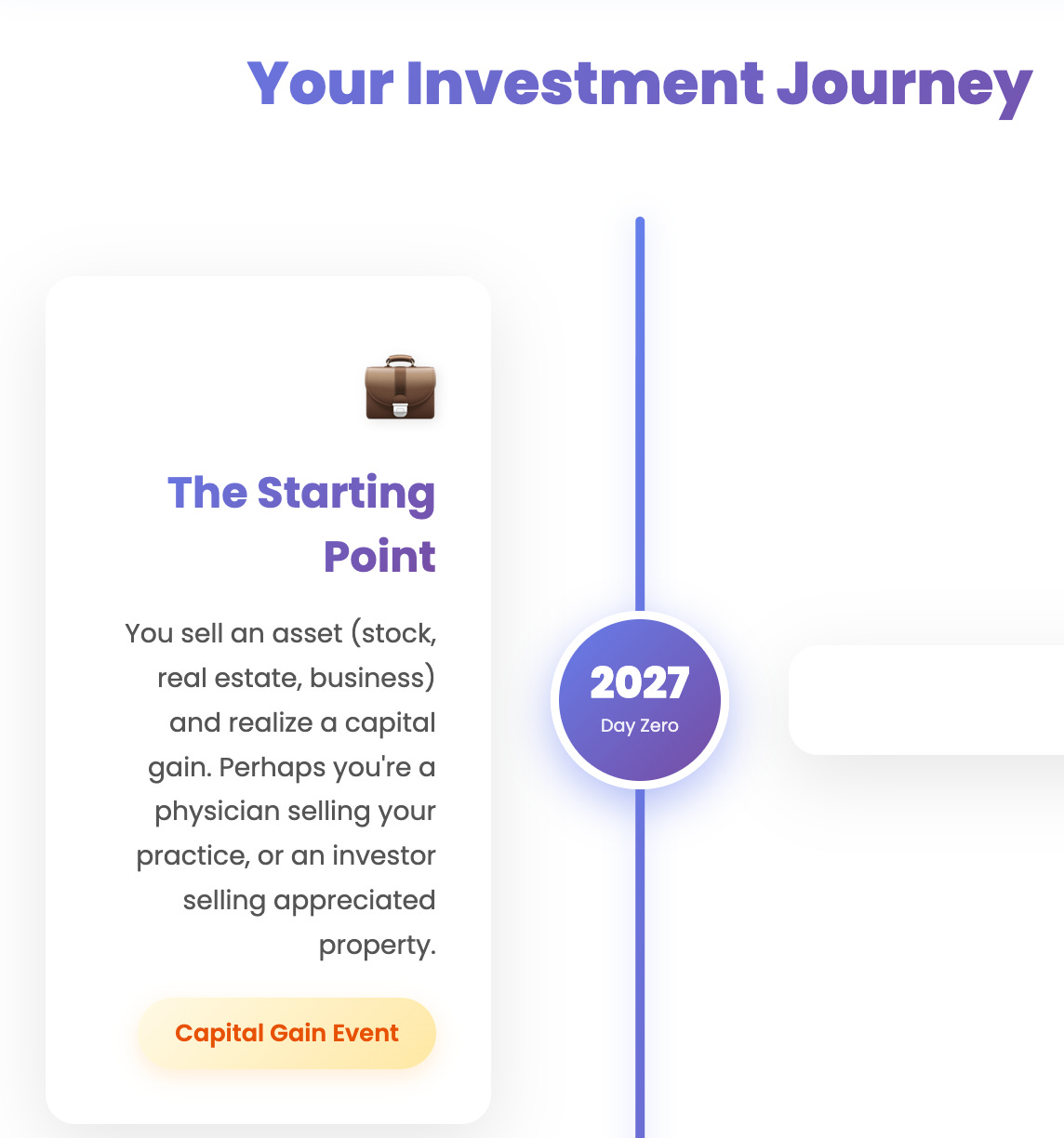

Day 0: The Capital Gain Event

It starts with a sale. You sell your medical practice, a rental property, stock holdings, or a business. Let’s say you’re Dr. Martinez, and you just sold your dermatology practice for $3 million with a $2 million capital gain.

Normally, you’d owe about $476,000 in combined federal and state capital gains taxes. But instead of writing that check to the IRS, you have another option: the QOF timeline.

What happens now: The 180-day clock starts ticking.

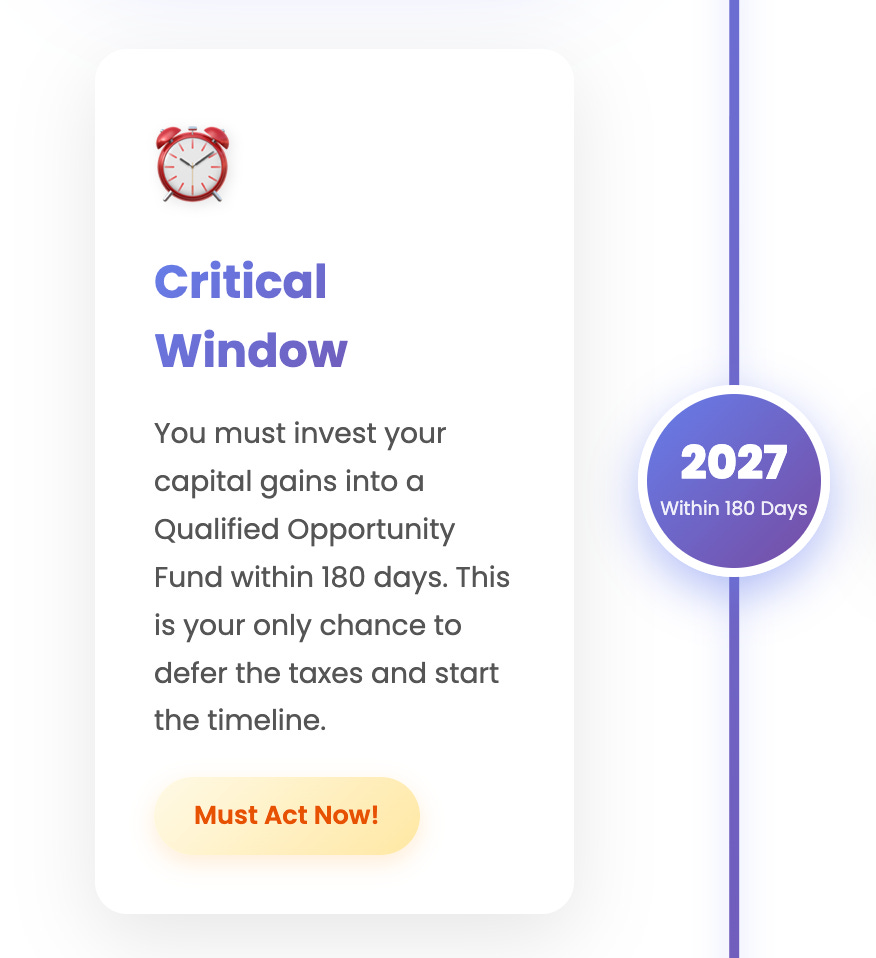

Days 1-180: The Critical Window

This is your only chance to enter the QOF program. You have exactly 180 days from your sale to invest your capital gains into a Qualified Opportunity Fund.

Miss this window by even one day? You lose access to all QOF benefits. There are no extensions, no exceptions, no do-overs.

What You Need to Do:

Research and select a QOF that aligns with your investment goals

Complete all paperwork and due diligence

Transfer your capital gains (not the full proceeds—just the gains) into the fund

Ensure the QOF provides proper documentation of your investment date

Critical Point: Only the capital gain amount qualifies for tax benefits. If you sell your practice for $3M with a $1M cost basis, you can invest the full $3M, but only the $2M gain receives QOF tax benefits.

What Happens If You Wait Too Long?

Let’s say you sell on January 1, 2027. Your 180-day deadline is June 30, 2027. If you invest on July 1? You pay the full capital gains tax immediately. The QOF opportunity is gone forever for that particular gain.

Timeline Checkpoint: By day 180, you’re officially in a QOF. Your taxes are now deferred, and the journey begins.

Years 1-5: The Growth Phase

Once your money is invested, you enter what I call the “patience phase.” Your capital is now:

Working: The QOF is developing real estate or investing in businesses within designated Opportunity Zones

Growing: Appreciation is building, but remains unrealized

Protected: Your original capital gains taxes are deferred—you don’t owe them yet

What’s Happening Behind the Scenes:

The QOF must maintain strict compliance:

Hold at least 90% of assets in Qualified Opportunity Zone Property

For existing properties, invest an amount equal to the purchase price in improvements within 30 months

Pass semi-annual asset tests

Maintain detailed records for IRS reporting

You don’t need to do anything during this phase except:

Monitor your investment statements

Ensure you’re maintaining records of your original investment date

Plan for the eventual tax payment in 2026

Real Example Timeline:

January 2027: Dr. Martinez invests $2M capital gain in a medical real estate QOF

February 2027: QOF purchases land in an Opportunity Zone

March 2027-December 2028: Development phase—construction of medical office buildings

2029-2031: Properties lease up, generating rental income

2032: Five years complete

Year 5: The First Milestone

At the 5-year mark, something important used to happen: investors who got in before 2021 received a 10% step-up in basis, meaning 10% of their original deferred gain became permanently tax-free.

For new investors entering in 2027 or later, this benefit no longer exists. The partial exclusions have expired. But you’re now halfway to the main prize.

Dr. Martinez’s Investment at Year 5 (2032):

Original investment: $2M

Current QOF value: ~$2.4M (assuming 4% annual growth)

Deferred tax still owed: Full amount on $2M (due Dec 2026)

Appreciation to date: $400K (still unrealized, still untaxed)

Years 6-9: Building Toward Tax-Free Status

You’re in the home stretch now. Your investment continues growing, and you’re building toward the most powerful benefit: complete tax-free appreciation.

What Makes These Years Important:

Every month that passes increases the eventual tax-free benefit. If your QOF doubles in value, you’re watching hundreds of thousands—or even millions—of dollars grow completely tax-free.

Dr. Martinez’s Investment at Year 8 (2035):

Original investment: $2M

Current QOF value: ~$2.9M

Taxes paid on original $2M gain: Paid in December 2026

Appreciation to date: $900K (still untaxed, approaching tax-free status)

Strategic Considerations During This Phase:

Don’t exit early: Selling before 10 years means losing the permanent exclusion benefit

Monitor fund performance: Ensure the QOF manager is executing the strategy effectively

Plan your exit: Start thinking about what you’ll do with the funds after year 10

Consider estate planning: If you pass away before year 10, your heirs receive a step-up in basis

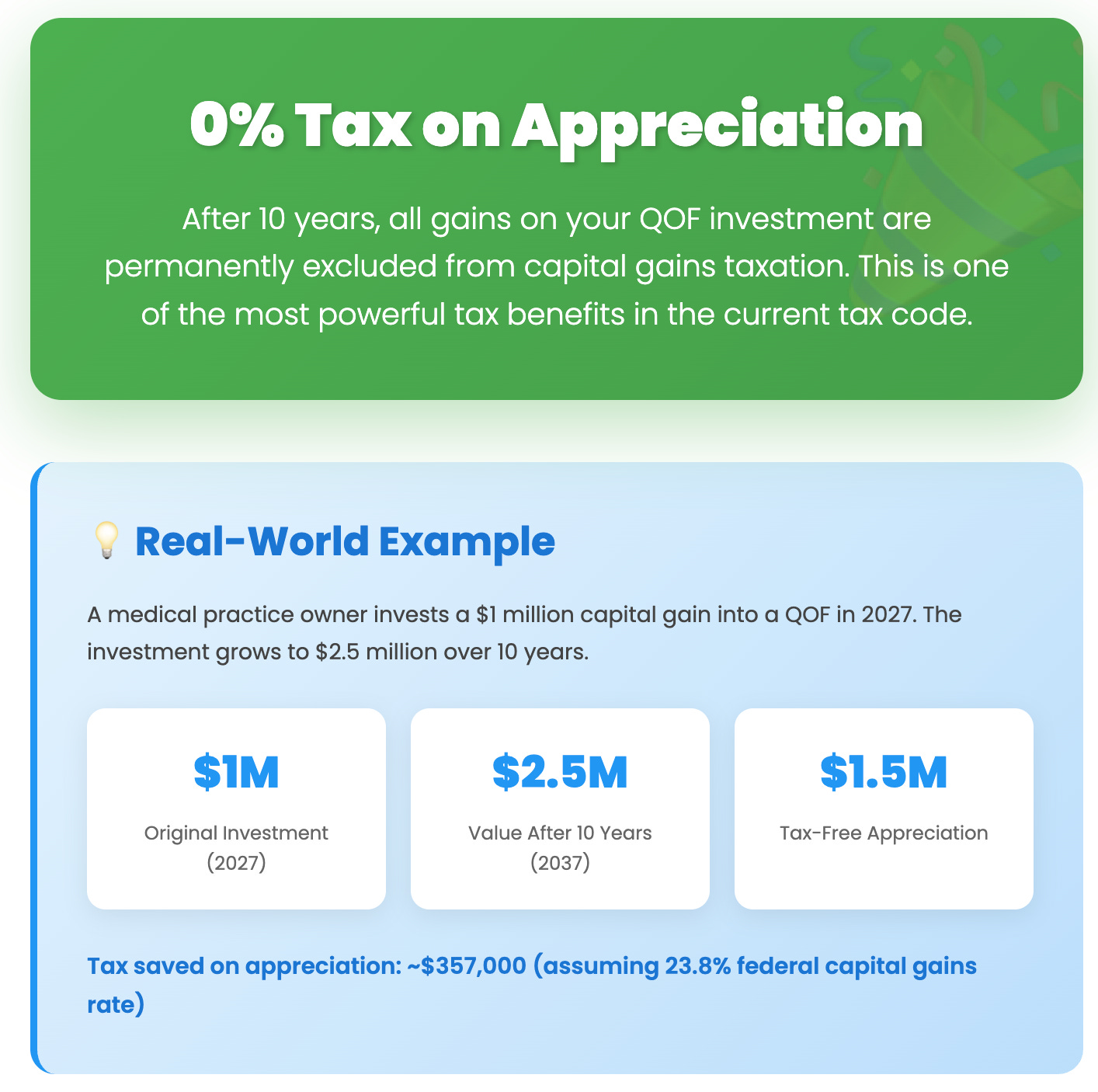

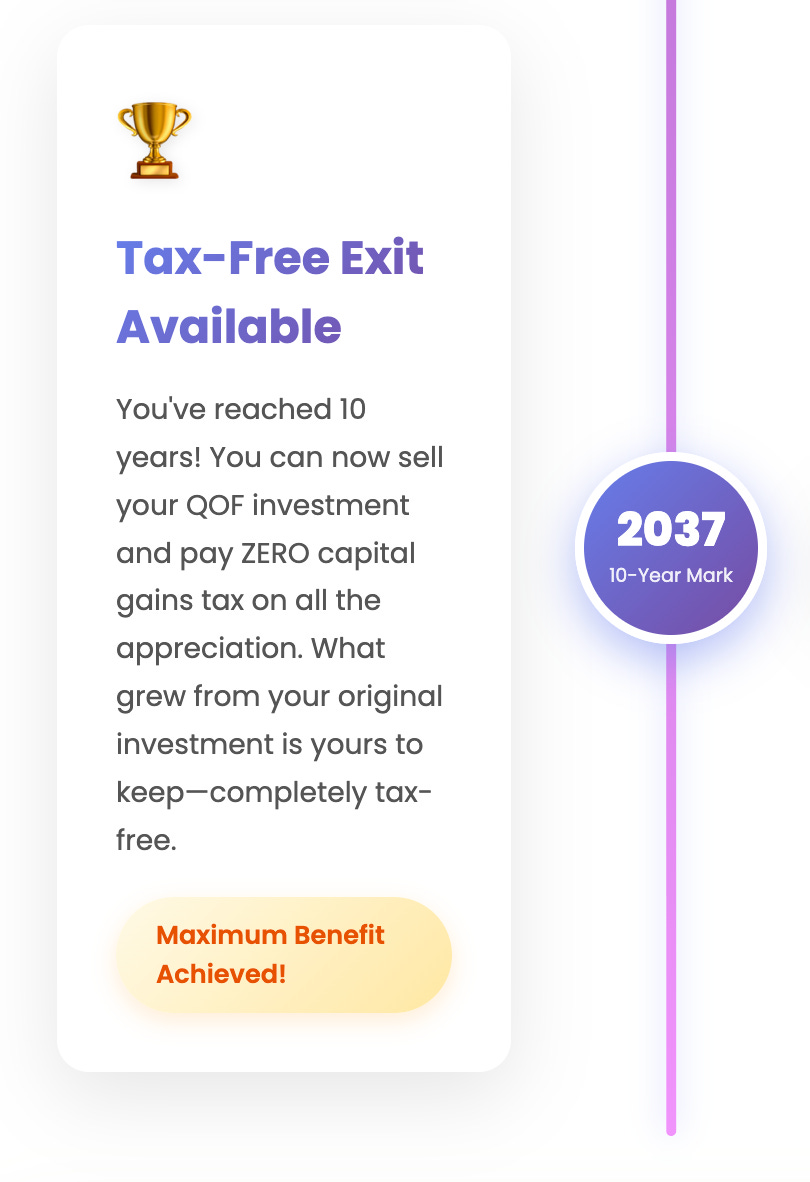

Year 10: The Golden Milestone

This is what you’ve been waiting for.

After holding your QOF investment for 10 years, you can exit and pay zero capital gains tax on all appreciation. Not reduced tax. Not deferred tax. Zero.

What Happens at the 10-Year Mark:

You have several options:

Sell your QOF investment and cash out: All appreciation is permanently tax-free

Take a “deemed sale” election: You can step up your basis in the investment without actually selling

Continue holding: There’s no requirement to exit at year 10; you can hold longer if you wish

Dr. Martinez’s Investment at Year 10 (2037):

Original investment: $2M

Current QOF value: $3.2M

Total appreciation: $1.2M

Tax owed on appreciation: $0

Tax savings: ~$285,600

The Math on Tax Savings:

Traditional investment: Pay ~23.8% on $1.2M appreciation = $285,600

QOF investment after 10 years: Pay $0

Total savings: $285,600

Plus, she had the benefit of deferring the original $476,000 tax bill from 2027 to 2026—essentially an interest-free loan from the government.

Special Timeline Scenarios

Scenario 1: What If You Die Before Year 10?

Your heirs inherit your QOF investment with a stepped-up basis. The original deferred gain disappears, and they can sell immediately with no tax on the appreciation to date. This makes QOFs particularly attractive for older investors in their 60s and 70s.

Scenario 2: What If You Need Money at Year 7?

You can sell, but you’ll pay capital gains tax on all appreciation. You’ve essentially wasted years 1-7 and given up the most valuable benefit. This is why QOFs only make sense if you’re certain about the 10-year commitment.

Scenario 3: What If the Investment Loses Money?

You still owe taxes on the original deferred gain (by December 2026 if you invested before then). The QOF loss doesn’t eliminate your original tax liability. This is a critical risk to understand.

The Complete Timeline at a Glance

Day 0: Realize capital gain

Day 180: Deadline to invest in QOF

December 31, 2026: Pay taxes on original deferred gain (if invested before 2027)

Year 5: Halfway point (partial exclusions expired for new investors)

Year 7: Three years until tax-free exit

Year 10: Eligible for complete tax-free exclusion on all appreciation

Year 10+: Can hold longer if desired, appreciation remains tax-free

Timeline Planning for 2027 and Beyond

If you’re reading this in 2027 or later, here’s your adjusted timeline:

Option A: Accept No Deferral, Focus on Appreciation

Sell asset and pay capital gains tax immediately

Invest remaining proceeds in QOF

Hold for 10 years

Exit with tax-free appreciation

Best for: Investors who expect strong returns and want to use after-tax capital efficiently

Option B: Wait for Future Gains

Save the QOF strategy for future capital gains events where the full timeline benefits can still be captured (if Congress extends the program).

Critical Timeline Mistakes to Avoid

Mistake #1: Miscounting the 180 Days

Count carefully. The clock starts on the date of sale, not the date you receive funds. If your sale closes on February 15, your deadline is August 14 (not August 15).

Mistake #2: Forgetting the December 2026 Deadline

You must have liquidity to pay the deferred taxes. This often catches investors off-guard. Plan ahead and set aside funds.

Mistake #3: Selling Just Before Year 10

Even selling at year 9 and 364 days means paying full capital gains tax on appreciation. Wait for the full 10 years.

Mistake #4: Not Documenting Your Timeline

Keep immaculate records of your investment date, amounts, and all correspondence. You’ll need these for IRS reporting and to prove your 10-year hold.

Your Personal Timeline Checklist

□ Identify your capital gain event and amount

□ Mark your 180-day deadline on the calendar

□ Research and select appropriate QOFs

□ Complete investment within 180-day window

□ Set reminder for December 31, 2026 (if applicable)

□ Set aside funds to pay deferred taxes

□ Monitor investment quarterly

□ Mark 10-year anniversary date

□ Plan exit strategy 6-12 months before year 10

□ Execute tax-free exit after 10 years

Time Is Everything

With Qualified Opportunity Funds, time literally equals money. The difference between 9 years and 10 years is hundreds of thousands of dollars in taxes. The difference between day 179 and day 181 is access to the entire program.

Understanding this timeline isn’t just helpful—it’s essential. Every milestone matters. Every deadline is firm. But if you navigate the timeline correctly, you can build substantial wealth completely free from capital gains taxation.

That’s the power of patient capital. That’s the power of the QOF timeline.