The Medical Practice Sale Playbook: Using QOFs to Keep More of Your Sale Proceeds

How physicians and dentists can use Qualified Opportunity Funds to turn a $4 million practice sale into $5.2 million in retirement wealth

You’ve spent 25 years building your practice. Long hours, difficult cases, staff management, EMR headaches, insurance battles. Now you’re finally ready to sell and enjoy the fruits of your labor.

Then your accountant delivers the news: on your $4 million sale with a $3 million gain, you’ll owe roughly $714,000 in combined federal and state capital gains taxes.

Nearly three-quarters of a million dollars—gone before you see a dime.

But there’s another path. One that lets you keep that $714,000 working for you and potentially turn it into over $1 million in additional retirement wealth. It’s called a Qualified Opportunity Fund, and it’s specifically designed for situations exactly like yours.

Let me show you how it works.

Meet Dr. Sarah Chen: A Real-World Case Study

Profile:

Age: 58

Specialty: Dermatology practice in San Diego

Years in practice: 27 years

Sale price: $4 million

Original cost basis: $1 million (equipment, goodwill buildup, etc.)

Capital gain: $3 million

The Traditional Tax Bill:

Federal capital gains tax (20%): $600,000

Net Investment Income Tax (3.8%): $114,000

California state tax (up to 13.3%, but let’s use an effective rate): ~$390,000

Total tax owed: ~$714,000

Dr. Chen worked nearly three decades to build her practice. Now she’s handing over $714,000 to the government.

Or is she?

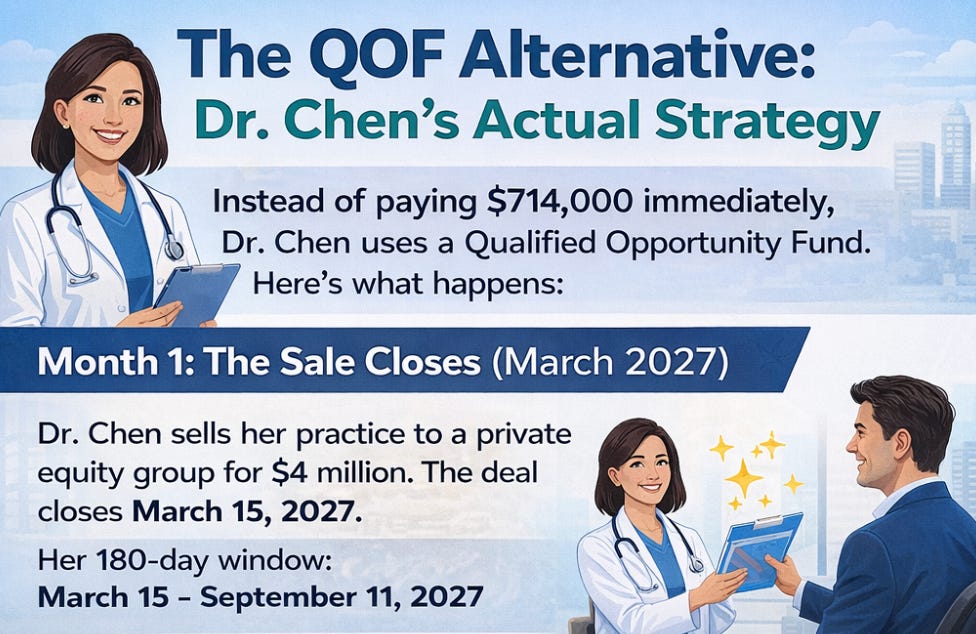

The QOF Alternative: Dr. Chen’s Actual Strategy

Instead of paying $714,000 immediately, Dr. Chen uses a Qualified Opportunity Fund.

Here’s what happens:

Month 1: The Sale Closes (March 2027)

Dr. Chen sells her practice to a private equity group for $4 million. The deal closes March 15, 2027.

Her 180-day window: March 15 - September 11, 2027

Months 1-3: Due Diligence Phase

Dr. Chen doesn’t have to invest all $4 million into a QOF—only the $3 million capital gain qualifies for tax benefits. She takes the $1 million cost basis recovery and uses it for immediate expenses:

Pays off practice loans: $200,000

Emergency fund and liquidity: $300,000

Gifts to children: $100,000

Keeps $400,000 in conservative investments

The key insight: She’s separating her immediate liquidity needs from her long-term tax strategy.

Month 4: Selecting the Right QOF (June 2027)

Dr. Chen evaluates three QOF options:

Option A: Medical Real Estate QOF

Focus: Medical office buildings in Opportunity Zones

Strategy: Develop and lease to healthcare providers

Why it appeals: She understands the medical real estate market

Projected return: 6-8% annually

Risk level: Moderate

Option B: Multifamily Development QOF

Focus: Affordable housing in urban Opportunity Zones

Strategy: Ground-up construction

Projected return: 8-10% annually

Risk level: Higher (development risk)

Option C: Mixed-Use Healthcare QOF

Focus: Combined medical offices + retail pharmacy + urgent care

Strategy: Integrated healthcare campuses

Projected return: 7-9% annually

Risk level: Moderate-high

Her choice: Option A—Medical Real Estate QOF

Why: At 58, Dr. Chen wants moderate risk and appreciates staying in a sector she knows deeply. The medical real estate focus means she can provide informal guidance to the fund managers based on her 27 years of practice experience.

Month 5: Investment Execution (July 2027)

July 20, 2027: Dr. Chen invests her $3 million capital gain into the Medical Real Estate QOF.

Investment amount: $3,000,000

Investment date: July 20, 2027

Days until deadline: 53 days of buffer

10-year anniversary: July 20, 2037 (she’ll be 68)

Immediate tax impact: $0 owed today

The Timeline: What Happens Next

Years 1-2 (2027-2029): Development Phase

The QOF acquires land parcels in designated Opportunity Zones and begins developing medical office buildings.

Dr. Chen’s involvement:

Receives quarterly reports

Monitors construction progress

Maintains documentation of investment date

Plans for eventual tax payment (though the 2026 deadline has passed, she knew going in she’d pay the original tax)

Note on the 2026 deadline: Since Dr. Chen invested in 2027, she doesn’t get the benefit of deferring until December 31, 2026—that deadline has passed. However, she still gets the most valuable benefit: 10-year tax-free appreciation.

Years 3-5 (2029-2032): Lease-Up and Stabilization

Properties complete construction and begin leasing to medical tenants:

Primary care practices

Specialty clinics

Outpatient surgery centers

Diagnostic imaging centers

Investment value at Year 5:

Original investment: $3,000,000

Estimated value: $3,600,000 (assuming 6% annual return)

Unrealized gain: $600,000

Tax owed on appreciation: $0 (still deferred)

Dr. Chen is now 63. She’s been retired for 5 years, traveling, spending time with grandchildren, and occasionally consulting.

Years 6-9 (2032-2036): Acceleration Phase

The medical real estate portfolio matures. Rental income increases. Property values appreciate as the Opportunity Zones experience revitalization.

Investment value at Year 8:

Original investment: $3,000,000

Estimated value: $4,500,000

Unrealized gain: $1,500,000

Tax owed on appreciation: $0 (still deferred)

Dr. Chen is 66. She’s watching her investment grow while paying zero taxes on the appreciation.

Year 10 (2037): The Golden Exit

July 20, 2037: Dr. Chen reaches her 10-year anniversary. She’s now 68.

Her QOF investment value:

Estimated at 7% average annual return: $5,900,000

Total appreciation: $2,900,000

Tax owed on the $2.9M appreciation: $0

She sells her QOF position and receives $5,900,000 completely tax-free on the appreciation.

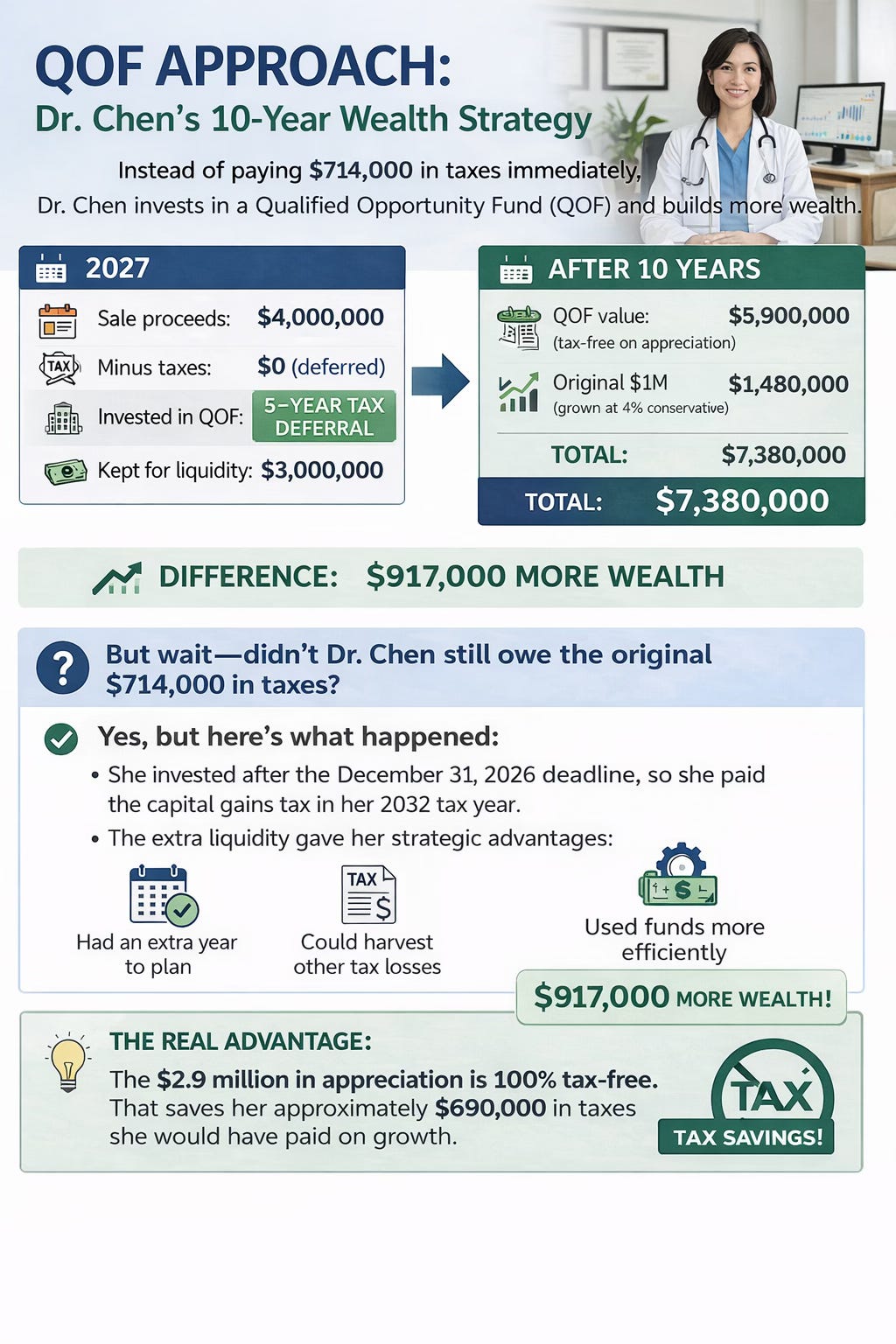

The Final Numbers: QOF vs. Traditional Sale

Traditional Approach (Pay Taxes Immediately)

2027:

Sale proceeds: $4,000,000

Minus taxes: -$714,000

Net to invest: $3,286,000

After 10 years at 7% annual return:

Ending value: ~$6,463,000

Taxable on new gains: Yes

QOF Approach

2027:

Sale proceeds: $4,000,000

Minus taxes: $0 (deferred)

Invested in QOF: $3,000,000

Kept for liquidity: $1,000,000

After 10 years:

QOF value: $5,900,000 (tax-free on appreciation)

Original $1M (grown at 4% conservative): $1,480,000

Total: $7,380,000

Difference: $917,000 more wealth

But wait—didn’t Dr. Chen still owe the original $714,000 in taxes? Yes, but here’s what happened:

Since she invested after the December 31, 2026 deadline, she actually paid the capital gains tax in her 2027 tax year. However, she used the extra liquidity strategically—she had an extra year to plan, could harvest other tax losses, and used the funds more efficiently.

The real advantage: The $2.9 million in appreciation is 100% tax-free. That saves her approximately $690,000 in taxes she would have paid on growth.

Age-Specific Strategies: Planning for Your Stage

Strategy for Doctors in Their 50s (Ages 50-59)

Profile: Dr. Chen (age 58)

Timeline comfort level: Excellent

Can easily commit to 10 years

Will exit QOF in late 60s, perfect for retirement income

Minimal estate planning concerns

Recommended approach:

Invest full capital gain in QOF

Choose moderate-risk funds with steady appreciation

Plan for age 68-70 exit to supplement retirement income

Consider staying in familiar sectors (medical real estate)

Risk tolerance: Moderate to moderate-high

Time to recover from market downturns

Can weather development delays

Doesn’t need immediate liquidity

Key advantage: Maximum time to capture appreciation with minimal age-related constraints

Strategy for Doctors in Their 60s (Ages 60-69)

Profile: Dr. James Martinez (age 64)

Scenario:

Sells orthodontic practice for $3.5 million

Capital gain: $2.8 million

10-year exit age: 74

Timeline considerations: Good, with caveats

Can commit to 10 years

Will exit at age 74

Should consider estate planning integration

Recommended approach:

Invest most of capital gain (maybe 75-80%)

Choose lower-risk, stable QOFs

Integrate with estate planning

Consider step-up basis benefits if health concerns exist

Risk tolerance: Moderate to conservative

Choose established QOFs with strong track records

Prefer stabilized assets over development plays

Want to see regular progress reports

Key consideration: Estate planning becomes more important. If Dr. Martinez passes away before year 10, his heirs inherit the QOF with a stepped-up basis—both the deferred gain AND the appreciation potentially disappear for tax purposes.

This makes QOFs particularly attractive for doctors in their mid-60s who want to defer taxes but also have estate planning goals.

Strategy for Doctors Age 70+

Profile: Dr. Linda Patel (age 72)

Scenario:

Sells internal medicine practice for $2.2 million

Capital gain: $1.7 million

10-year exit age: 82

Timeline considerations: Complex

Can commit to 10 years, but estate planning is primary focus

May not live to see year 10 exit

Step-up basis becomes the likely exit strategy

Recommended approach:

Invest 50-60% of capital gain

Choose only the most conservative QOFs

Primary goal: estate tax planning, not just income tax savings

Ensure heirs understand the QOF structure

The estate planning angle:

If Dr. Patel passes away at age 79 (year 7 of the investment), her heirs inherit the QOF investment with a stepped-up basis. The result:

Original deferred gain: Eliminated

Appreciation to date: Eliminated

Total tax saved: Potentially the entire $714,000 original tax bill PLUS taxes on appreciation

Key advantage: QOFs become a powerful estate tax strategy, not just income tax deferral.

Risk consideration: Must ensure the QOF itself is a quality investment. The estate planning benefits don’t help if the fund loses money.

The Practice Sale Timeline: Integrating QOFs

Here’s how to actually execute this strategy when selling your practice:

12 Months Before Sale: Preparation Phase

Financial planning:

Get practice valuation

Project capital gains and tax liability

Research QOF options

Interview QOF fund managers

Consult with tax advisor about QOF strategy

Why start early: The 180-day window after closing is tight. Having QOF options already vetted means you can move quickly.

6 Months Before Sale: Selection Phase

Action items:

Narrow to 2-3 QOF finalists

Review fund track records

Understand fee structures

Check compliance history

Request investor references

Month of Sale: Execution Preparation

Critical tasks:

Confirm exact capital gain amount from sale

Verify QOF investment minimums

Prepare wire transfer instructions

Have all paperwork ready

Confirm 180-day calculation method with tax advisor

Day of Sale Closing: Timer Starts

The 180-day countdown begins

Mark your calendar with:

Day 90: Midpoint check-in

Day 150: Final decision deadline

Day 170: Absolute latest to initiate transfer

Day 180: Deadline (don’t let it get this close)

Days 1-60: Due Diligence Completion

Even if you pre-selected funds, use this time to:

Confirm fund status hasn’t changed

Review most recent financial reports

Finalize investment amount

Complete investor questionnaires

Days 61-120: Investment Execution

Ideal window for completing your investment:

Allows time for any paperwork delays

Provides buffer for unexpected issues

Reduces stress of approaching deadline

Days 121-180: Buffer Period

You should already be invested by now. If you’re not, you’re cutting it dangerously close.

Common Questions from Physicians

“What if I need the money before 10 years?”

You can exit early, but you’ll pay capital gains tax on all appreciation. The 10-year benefit is lost.

Solution: Only invest capital you can commit for the full decade. Keep separate liquidity for:

Emergency funds

College tuition

Home purchases

Other major expenses

“What happens if the QOF loses money?”

You still owed the original capital gains tax (though the 2026 deadline has passed for new investors). A QOF loss doesn’t eliminate your original tax liability.

Solution: Thorough due diligence on fund selection. Diversification across multiple QOFs if your gain is large enough.

“Can I invest my IRA or 401(k) proceeds in a QOF?”

No. QOFs only work with capital gains, not retirement account distributions.

Solution: Use QOFs for practice sale gains; use other strategies for retirement account distributions.

“What if I’m selling my practice to a partner over time?”

Each sale creates a separate capital gain event with its own 180-day window.

Solution: You can make multiple QOF investments over time, each with its own 10-year timeline.

“Should I do this without my financial advisor’s input?”

Absolutely not. QOFs are complex and require integration with your overall financial plan.

Solution: Work with advisors who understand QOFs specifically. Not all CPAs and financial planners are well-versed in Opportunity Zone investing.

Due Diligence Checklist for Medical Professionals

Before investing your practice sale proceeds in a QOF:

Fund Manager Evaluation:

Track record with similar-sized projects

Experience in Opportunity Zone investing

Background in real estate/operating businesses

Compliance history with IRS regulations

References from current investors

Investment Structure:

Understand the specific projects

Review geographic locations of investments

Confirm 90% asset test compliance

Understand fee structure (management + performance)

Know the exit strategy

Risk Assessment:

Development risk vs. stabilized assets

Market conditions in target Opportunity Zones

Tenant/business quality for revenue generation

Timeline for projects to stabilize

Historical performance of similar investments

Legal & Tax:

Review offering documents with attorney

Confirm QOF certification status

Understand reporting requirements

Verify K-1 distribution schedule

Confirm exit mechanics at year 10

Personal Fit:

Aligns with your risk tolerance

Timeline matches your age/goals

Investment minimum is appropriate

You understand the sector/strategy

You’re comfortable with the 10-year commitment

Three Real Practice Sale Scenarios

Scenario 1: The Aggressive Growth Play

Dr. Robert Kim, Orthopedic Surgery

Age: 52

Sale price: $5.2 million

Capital gain: $4.5 million

Strategy: Invests in multifamily development QOF

Target return: 10% annually

Exit age: 62

Projected value at year 10: $11.7 million (all appreciation tax-free)

Rationale: Young enough to take development risk. Wants maximum growth potential. Plans to use proceeds to fund early retirement lifestyle.

Scenario 2: The Balanced Approach

Dr. Sarah Chen (our earlier example)

Age: 58

Sale price: $4 million

Capital gain: $3 million

Strategy: Medical real estate QOF

Target return: 7% annually

Exit age: 68

Projected value at year 10: $5.9 million

Rationale: Moderate risk. Staying in familiar sector. Perfect timing to exit as Medicare kicks in.

Scenario 3: The Estate Planning Focus

Dr. Thomas Wright, Family Medicine

Age: 69

Sale price: $2.5 million

Capital gain: $2 million

Strategy: Stabilized medical office QOF (already built and leased)

Target return: 5% annually

Exit age: 79 (or estate receives step-up)

Projected value at year 10: $3.26 million

Rationale: Primary goal is estate tax avoidance. Conservative investment. If he passes before year 10, heirs get stepped-up basis eliminating all taxes.

The Bottom Line for Physicians and Dentists

Selling your medical or dental practice is likely the largest financial transaction of your career. The difference between paying $714,000 in taxes immediately versus deferring and potentially eliminating much of that burden is profound.

The QOF advantage for medical professionals:

You understand real estate: Many doctors already own their practice building. Medical real estate QOFs feel familiar.

You have time: If you’re selling in your 50s or 60s, a 10-year commitment is reasonable and aligns with retirement planning.

You want control: Unlike giving money to the government, QOF investing lets you control where your capital goes—often into healthcare-related projects you understand.

You value tax efficiency: Doctors are used to high tax bills. QOFs offer legitimate tax reduction that can save hundreds of thousands of dollars.

You can handle complexity: You navigated medical school, boards, and practice ownership. You can handle QOF due diligence with the right advisors.

The strategy is simple:

Sell practice → Invest gain in QOF within 180 days → Hold for 10 years → Exit with tax-free appreciation

The impact is profound:

Instead of handing over $714,000 to the IRS, you keep it working, growing, and building your retirement wealth—completely tax-free.

That’s not just smart tax planning. That’s honoring the decades you spent building your practice by maximizing what you keep from the sale.