Medical Practice Sale Playbook using QOFs

You’ve spent three decades building something remarkable. Your practice is your life’s work — the late nights, the patient relationships, the staff you’ve mentored. And now, a private equity group or DSO is offering you $4 million.

It should be a triumphant moment. But between federal capital gains tax, state income tax, and the net investment income surtax, over 30 cents of every dollar can evaporate before you see it. For a $4 million sale, that’s potentially $1.2–1.4 million paid to the IRS.

Most doctors accept this as inevitable. The ones working with sophisticated advisors don’t — and the ones who are willing to plan 18 to 36 months ahead and time their exit strategically are in an even better position.

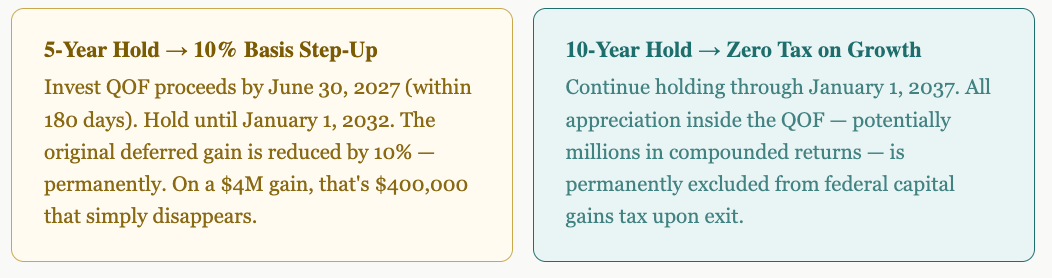

Qualified Opportunity Funds (QOFs) are among the most powerful tools available to physicians selling a practice. And for doctors who can time their sale to January 1, 2027, the combination of a 5-year deferral, a step-up in basis, and a 10-year appreciation exclusion creates a tax outcome that simply cannot be replicated with any other single strategy.

Legislative note: The QOF program's original deferral window closes December 31, 2026 for investments to qualify for the 5-year step-up. This article models a January 1, 2027 sale under anticipated QOF legislation renewal — a provision with strong bipartisan support that many tax practitioners expect Congress to extend as part of broader tax legislation. Your advisor should confirm current law before executing. All scenarios below assume renewed QOF provisions on terms substantially similar to the original program.

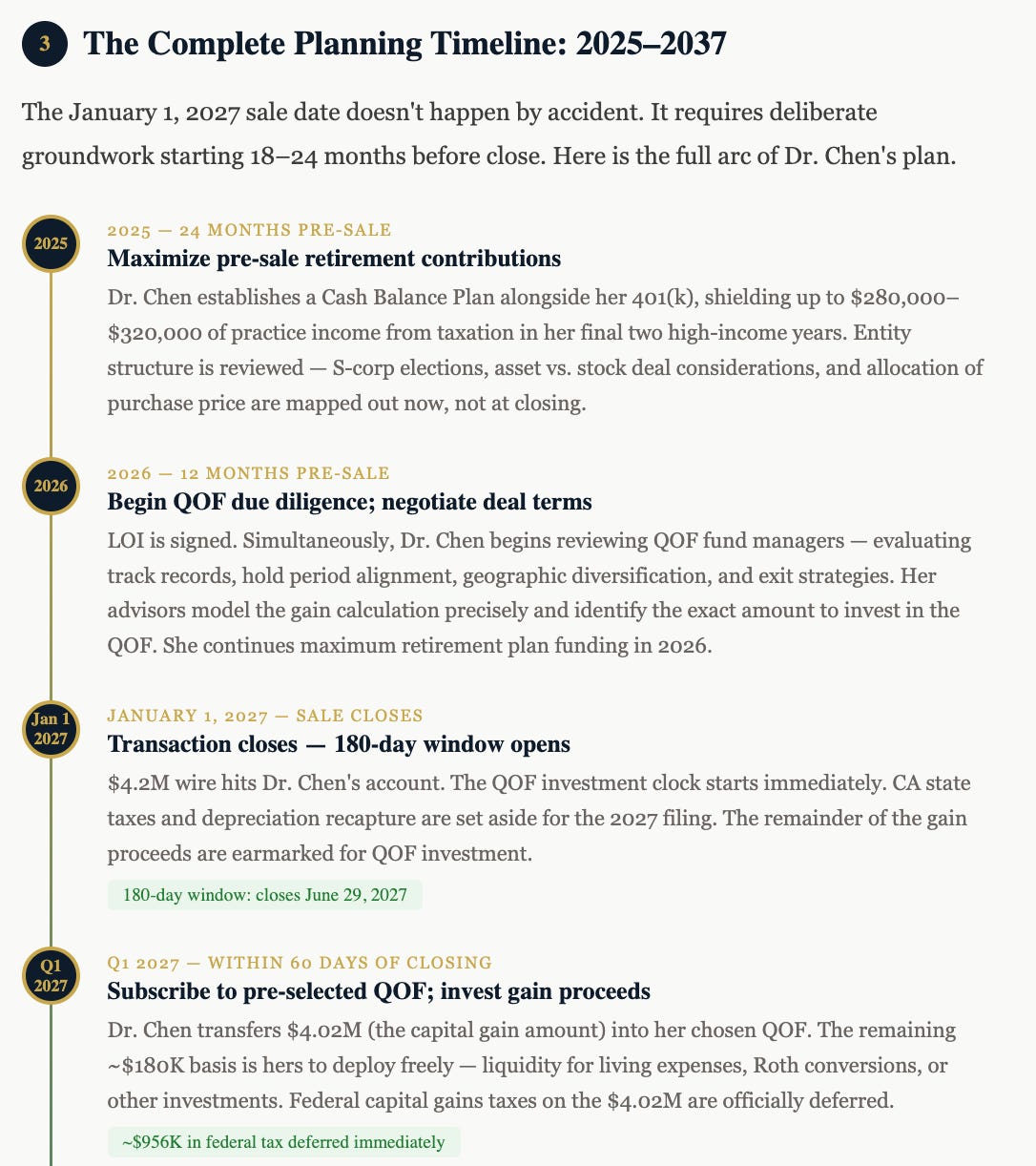

Why January 1, 2027 Is the Magic Date

Not all QOF timing is equal. The program has always rewarded patience — specifically, investors who hold long enough to unlock each successive benefit tier. A January 1, 2027 sale positions Dr. Chen to access all three benefit layers simultaneously.

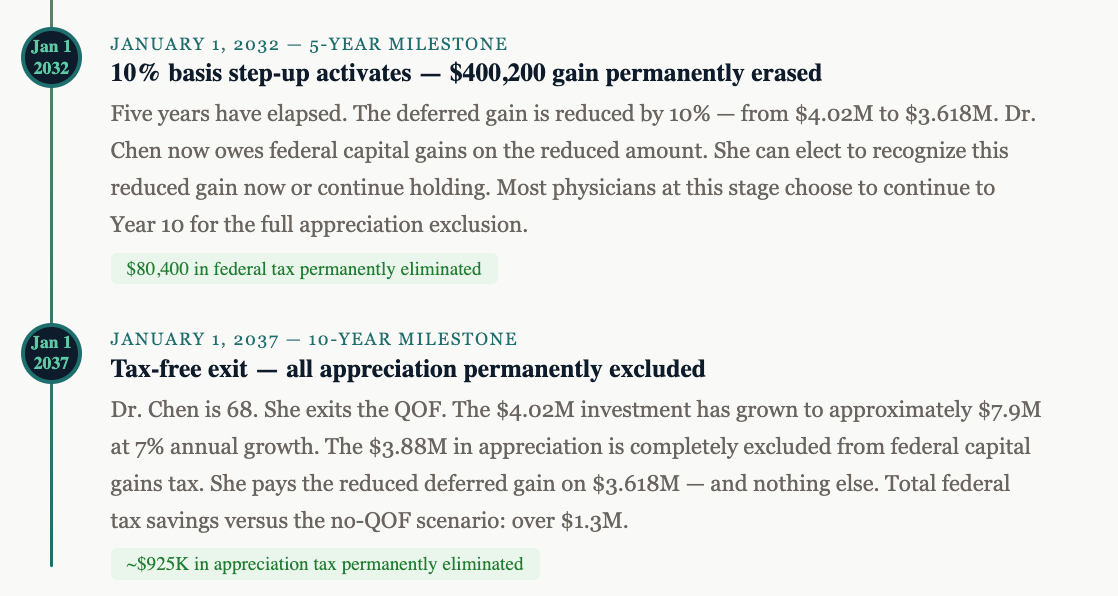

The 5-year step-up is particularly significant. Unlike most tax benefits that merely delay the inevitable, this one permanently reduces the taxable gain. Combined with five years of tax-free compounding on capital that would otherwise have gone to the IRS, the January 1, 2027 timing is the optimal entry point for a doctor in their late 50s.

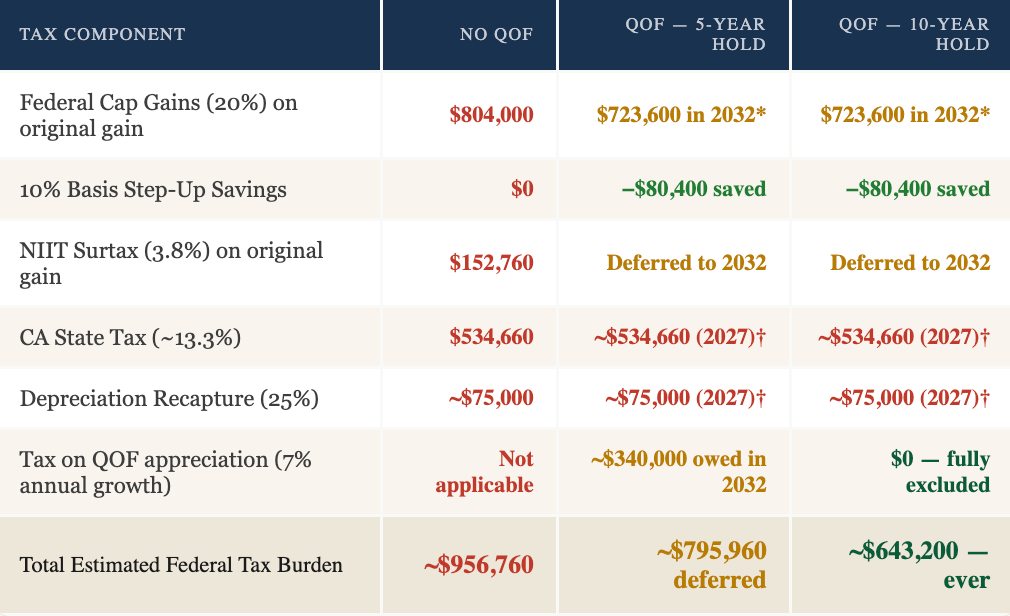

Dr. Chen’s $4.02M capital gain faces a brutal effective tax rate: 20% federal long-term capital gains + 3.8% NIIT + California’s 13.3% state rate. That’s a blended rate approaching 37% — or roughly $1.49M owed if she does nothing.

By investing her gain proceeds into a QOF within 180 days of closing, Dr. Chen activates the full three-tier benefit stack. Here’s how the numbers compare across three scenarios:

*Deferred federal gain recognized at 5-year mark (2032), reduced by 10% step-up. †California does not conform to federal QOF deferral; CA state taxes and depreciation recapture are generally owed in the year of sale. QOF appreciation modeled at 7% annual growth over 10 years on $4.02M invested. All figures illustrative; individual results will vary.

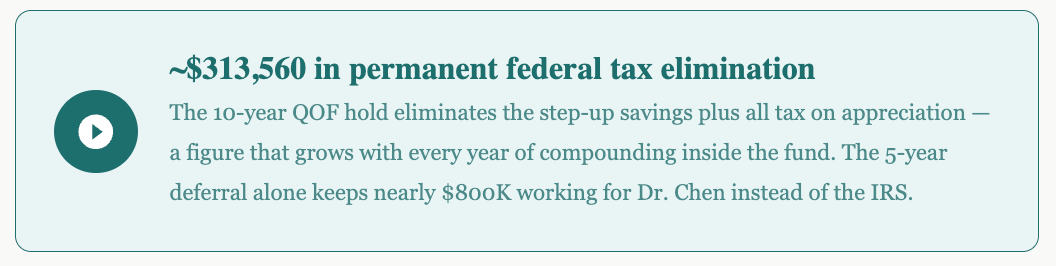

To put the 10-year exclusion in concrete terms: $4.02M compounding at 7% annually for 10 years grows to approximately $7.9M. Without the QOF, that $3.88M in appreciation would trigger another ~$925,000 in federal capital gains and NIIT. With the 10-year hold, that bill is zero.

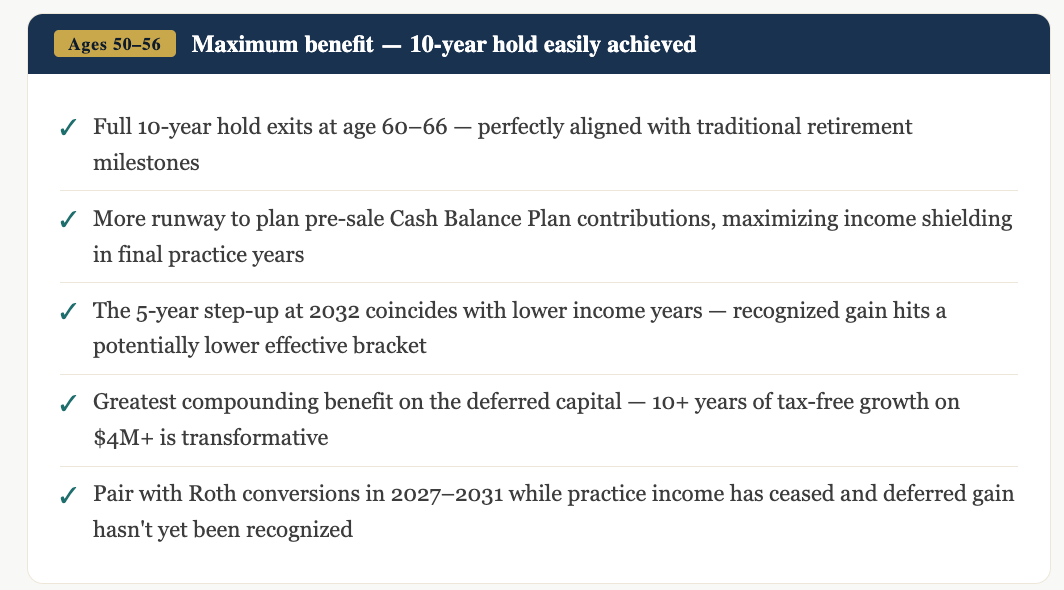

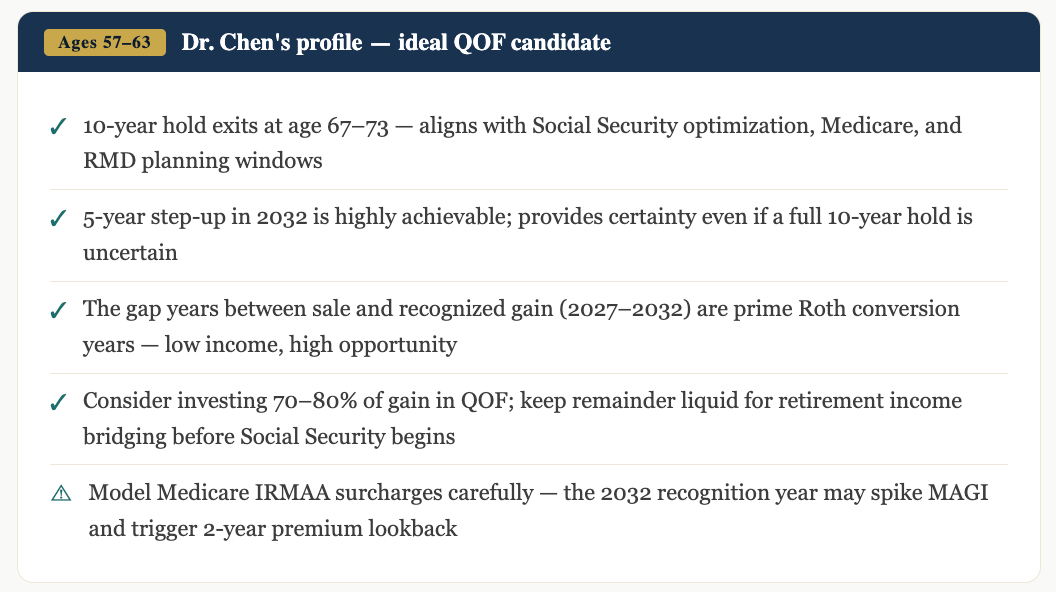

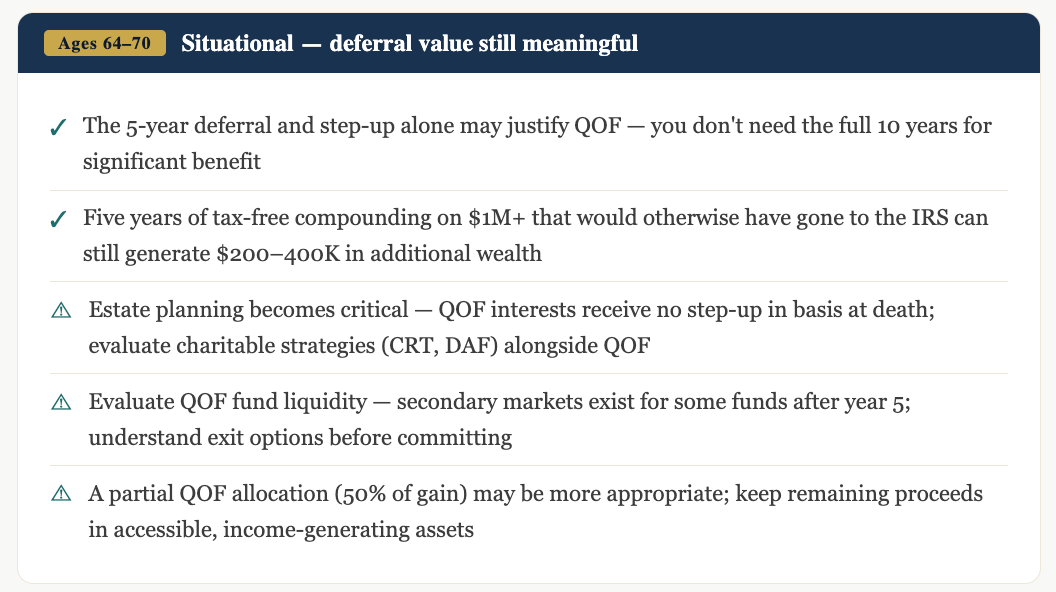

Timeline Planning by Age

The January 1, 2027 strategy is optimized for physicians in their mid-to-late 50s. But the QOF framework has meaningful applications across a wider age range. Here’s how the math and strategy shift by decade.