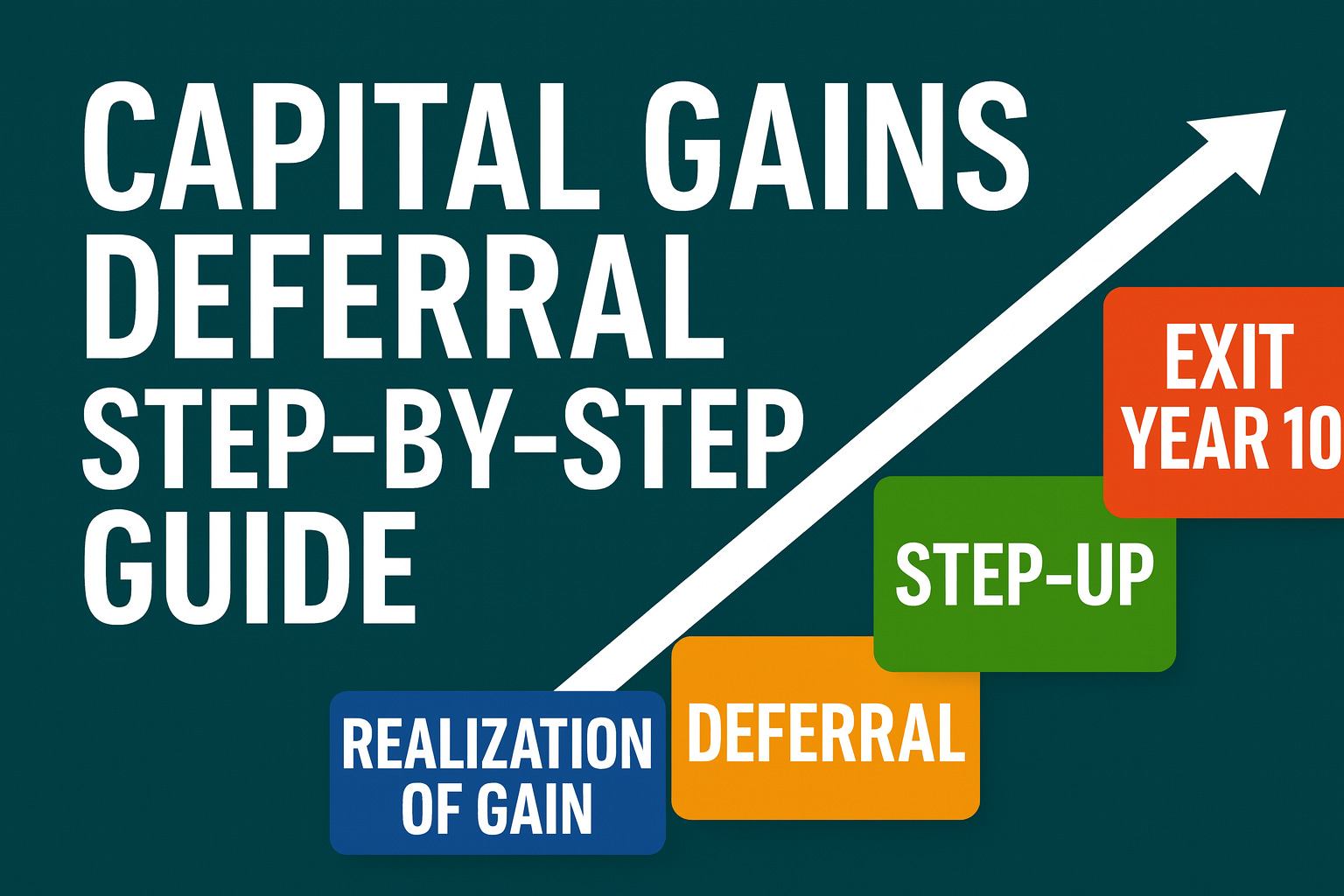

How Capital Gains Deferral Through QOFs Works (Step-by-Step Guide)

Qualified Opportunity Funds (QOFs) offer one of the most powerful tools in modern tax strategy — the ability to defer, reduce, and potentially eliminate capital gains taxes. Created under the 2017 Tax Cuts and Jobs Act, QOFs channel investment into designated Opportunity Zones (OZs), while rewarding investors for long-term participation. Here’s a clear, step-by-step look at how the process works from start to finish.

1. Realization of a Capital Gain

Everything begins with a realization event — selling an asset such as stock, real estate, a business, or even cryptocurrency. Normally, that sale would trigger an immediate capital gains tax due in the year of sale.

However, under the QOF rules (26 U.S.C. §1400Z-2), an investor can defer recognizing that gain if they reinvest it into a Qualified Opportunity Fund within a specific window of time.

Example: You sell a rental property on June 1, 2025, and realize a $500,000 capital gain. Instead of paying tax in 2025, you can elect to defer that gain by investing in a QOF.

“Deferring capital gains isn’t just about tax savings — it’s about redeploying idle capital into projects that create jobs, build infrastructure, and compound real wealth over time.”

— Robert Mowry, Senior Partner, Qualified Opportunity Fund

2. The 180-Day Investment Window

The IRS gives investors 180 days from the date of realizing the gain to reinvest the amount of the gain (not necessarily the entire sale proceeds) into a QOF.

For individuals, that 180-day clock starts on the sale date. For pass-through entities like partnerships or S-corps, investors can elect to start the clock either on:

the date the entity realized the gain, or

the end of the entity’s tax year.

Missing this window forfeits the deferral opportunity — so timing and documentation are critical.

3. Deferral of the Original Gain

Once the reinvestment is made, that original capital gain is deferred — meaning no tax is owed until the earlier of:

the date the QOF investment is sold or exchanged, or

December 31, 2026, the statutory deadline for all deferred gains.

While the deferral clock ends in 2026, investors can continue to hold the QOF investment beyond that date, and the appreciation on the QOF itself becomes the next tax benefit.

“A well-structured QOF turns a one-time tax event into a decade-long growth engine. The real opportunity lies in pairing smart timing with mission-driven investment.”

— Robert Mowry, Senior Partner, Qualified Opportunity Fund

4. Step-Up in Basis

Originally, investors received up to a 15% or 10% basis step-up for holding periods of 7 or 5 years before 2026. That benefit phased out as we approached 2027, but Congress is currently considering “Opportunity Zone 2.0” legislation that could restore it.

Even without it, the investor still benefits from deferral through 2026 and the complete exclusion of appreciation if the QOF is held for at least ten years.

5. Exit After Year 10 – Tax-Free Appreciation

The final stage is where the QOF structure truly shines. If the investor holds the QOF investment for 10 years or longer, they can elect a basis step-up to fair market value when exiting.

That means all appreciation inside the QOF — the growth on your investment — is permanently tax-free.

Returning to our example: if your $500,000 deferred gain grows to $1 million by 2035, you’ll owe no tax on that additional $500,000 when you sell.

Summary

QOFs transform capital gains from a tax liability into an engine for long-term, tax-advantaged growth.

Realize a gain.

Reinvest within 180 days.

Defer the tax until 2026 or sale.

Enjoy step-ups and potential reductions.

Exit after 10 years tax-free.

For investors, advisors, and fund managers alike, understanding these mechanics isn’t just about compliance — it’s about capturing one of the most remarkable opportunities in modern tax law.